THE COMPLETE GUIDE TO REAL ESTATE AGENT FINANCIAL SYSTEMS

Learn how to build a simple financial system for your real estate business to track closings, expenses, and mileage while staying organized year-round.

03/10/2026 | 12 Minute Read

By: Christian Tiessen

Introduction

Every successful real estate business eventually runs on systems.

At first, many agents rely mostly on effort and memory to keep things moving. But as your business grows, it becomes harder to manage everything without structure. The most organized agents gradually build systems that support different parts of their business.

Common systems real estate agents develop include:

lead generation systems

marketing and advertising systems

client communication systems

transaction management systems

administrative workflows

financial tracking systems

Each system brings consistency and organization to a specific part of the business.

For example, a lead generation system might define how you follow up with new prospects. A transaction system might outline how contracts, deadlines, and documents are handled after a deal goes under contract.

But one system that many agents overlook is their financial system.

Instead of using a consistent structure, financial information often ends up scattered across multiple places:

spreadsheets

emails

notes apps

paper receipts

bank statements

or sometimes just memory

Over time this creates confusion about important questions such as:

How much income have I actually earned this year?

What expenses have I deducted?

How profitable is my business?

What will I owe in taxes?

Without a system, the financial side of a real estate business becomes difficult to understand and manage.

The good news is that a financial system does not need to be complicated. In most cases, it simply means creating a clear structure for organizing the financial activity of your business.

In this guide, we’ll explain:

what a financial system for real estate agents looks like

why it matters

the habits that make it work

how you can stay organized year-round

What Is a Financial System for a Real Estate Agent?

A financial system is simply the structure you use to organize and track the financial activity of your business.

Instead of having financial information scattered across multiple places, everything follows a consistent structure.

A well-organized financial system allows you to easily track:

closings and commission income

business expenses

mileage related to real estate activities

financial trends over time

The goal is not complex bookkeeping or hours at your computer.

The goal is clarity.

When you can clearly see how money flows through your business, it becomes much easier to understand performance and make informed decisions.

Without a system, agents often have to piece together financial information from multiple sources. This leads to missing data, incomplete records, and unnecessary stress during tax season.

A simple system eliminates much of that confusion.

Why Many Real Estate Agents Never Build a Financial System

Despite the benefits, many agents never build a formal financial system.

Often the reason is not lack of ability, but lack of focus.

Most agents enter the real estate industry because they enjoy:

working with clients

negotiating deals

helping people buy and sell homes

Financial organization rarely feels like the most exciting part of the job.

In addition, financial management can feel intimidating. Spreadsheets can be frustrating to maintain, and traditional accounting software often feels overly complicated for a commission-based business.

Because of this, financial organization often gets pushed aside while agents focus on client work and transactions.

This hesitation is extremely common among real estate professionals.

Over time, the lack of a system makes financial tracking feel even more overwhelming. The longer it’s delayed, the harder it feels to get started.

Why Real Estate Agents Need a Financial System

Operating without a financial system creates several challenges.

When financial information is scattered or incomplete:

expenses often go untracked

records become inconsistent

financial visibility disappears

Without clear records, it becomes difficult to answer important business questions like:

How profitable is my real estate business?

Where is my money going each month?

How much should I set aside for taxes?

When you lack visibility into your finances, you often end up making business decisions without reliable information.

For example, you might spend heavily on marketing without knowing whether those expenses are actually producing results. Or you may overestimate your tax obligations because you do not have accurate records of your income and deductions.

These problems often surface during tax season, when agents must scramble to reconstruct an entire year of financial activity.

A financial system helps prevent this situation by keeping records organized throughout the year.

Read more about Why Real Estate Agents Need a Financial System to Stay Organized

A financial system also creates several benefits.

When your numbers are organized, you gain visibility into how your business actually operates.

For example, you might notice patterns such as:

certain months consistently producing more closings

marketing strategies that generate better returns

expenses that are gradually increasing over time

Without a system, these patterns are almost impossible to see.

But when your financial information is organized, you can quickly review your numbers and understand how your business is performing.

For many agents, simply having organized financial records creates a sense of relief. Instead of wondering where things stand, you can open your system and immediately see the numbers that matter.

Why Most Financial Tracking Methods Fail Real Estate Agents

Many agents recognize the need to track their finances and attempt to create their own system.

Common methods include:

spreadsheets

notes apps

folders of receipts

generic accounting software

While these methods can work in theory, they often become difficult to maintain in practice.

Spreadsheets require constant manual updates or figuring out complex formulas. Notes apps quickly become disorganized. Paper receipts are easy to lose. And many accounting platforms are designed for traditional businesses rather than commission-based professionals.

Because these systems require so much manual effort, agents often abandon them after a few months or never even start in the first place.

Consistency becomes the biggest challenge.

A financial system only works when it can be maintained easily throughout the year.

The Structure of a Simple Real Estate Financial System

Fortunately, a financial system for real estate agents does not need to track dozens of categories.

In most cases, you only need to focus on three core areas:

Closings

Expenses

Mileage

Together, these three categories create a clear picture of how your business is performing.

Closings

Closings represent the revenue side of your real estate business.

Tracking closings allows you to monitor:

transaction details

commission income

production over time

By recording this information consistently, you can easily review your performance throughout the years and identify patterns in your business activity.

Expenses

As an independent contractor, you operate as a small business owner.

This means many of the costs associated with running your real estate business may qualify as deductible expenses.

Common examples include:

marketing and advertising

website and CRM tools

listing signs and lockboxes

professional memberships and licensing fees

According to the National Association of Realtors, agents spend thousands of dollars annually on marketing, transportation, and professional services.

Tracking expenses throughout the year ensures you have accurate records when preparing your taxes.

Mileage

Driving is another major component of a real estate agent’s work.

You may drive regularly to:

property showings

listing appointments

property tours

open houses

inspections

These miles can often be deducted as a business expense when properly documented. The IRS publishes a standard mileage deduction rate each year for business driving.

Because real estate agents spend significant time driving, tracking mileage consistently can result in substantial deductions.

When closings, expenses, and mileage are tracked together, you gain a clear financial picture of your business.

How Real Estate Agents Can Build a Financial System

Many agents assume they need to create the perfect financial system right away.

In reality, most systems evolve gradually over time.

A practical starting point is documenting your current financial process.

Ask yourself questions such as:

Where do I currently track my closings?

How do I record expenses?

Where do receipts go?

How am I tracking mileage?

Writing down your current process helps reveal where financial information already exists and where gaps may be occurring.

From there, you can begin simplifying and improving the structure.

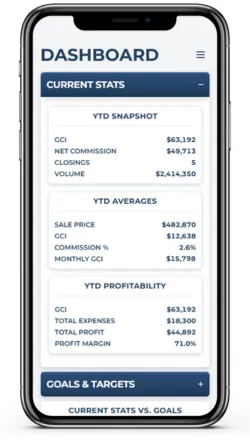

For example, an agent might decide to consolidate financial tracking into a single location like LEDGNT instead of using multiple spreadsheets and notes apps.

It’s also helpful to periodically review how well your system is working.

Questions to consider include:

Is it easy to record new expenses?

Am I consistently tracking mileage?

Can I quickly see my financial numbers?

Most business systems require small adjustments before they work smoothly.

Very few systems are perfect on the first attempt.

The goal is not perfection, but gradual improvement.

The Habits That Keep Financial Systems Working

Even the best financial system will fail if it is not maintained consistently.

Fortunately, financial organization does not require hours of bookkeeping each week.

Many organized agents rely on a few simple habits.

Weekly financial check-ins

Spending a few minutes reviewing your financial activity each week helps keep records accurate and up to date.

Recording expenses immediately

Entering expenses when they occur prevents you from forgetting them later.

Uploading receipts regularly

Keeping digital copies of receipts ensures important documentation is not lost.

These habits help maintain organization throughout the year rather than scrambling to catch up later.

Agents who maintain these routines tend to stay far more organized and less stressed over time.

Common Financial Organization Mistakes Real Estate Agents Make

Even agents who attempt to track their finances often run into common problems.

Mixing business and personal finances

Using the same account for both personal and business purchases can make financial records difficult to separate.

For example, imagine reviewing a bank statement that includes groceries, gas, marketing ads, client lunches, and personal purchases all mixed together.

Trying to determine which expenses belong to the business quickly becomes frustrating, and some deductions may be missed entirely.

Tracking inconsistently

Some agents track expenses for a few months but eventually stop updating their records.

This often happens during busy seasons when transactions and client work take priority. By the time you try to catch up, weeks or months of financial activity may be missing.

At that point it becomes difficult to remember what each purchase was for.

Relying on memory

Trying to remember expenses or mileage weeks later almost always leads to missing information.

For example, you might remember driving to several listing appointments last month, but recalling the exact dates and miles becomes nearly impossible.

Waiting until tax season

Attempting to organize an entire year of financial activity during tax season creates unnecessary stress.

You recognize this situation: digging through email receipts, scanning old bank statements, and trying to remember expenses from months earlier.

A consistent system throughout the year prevents this problem entirely.

The Small Business Administration recommends maintaining accurate financial records throughout the year to help small business owners stay organized and prepared for taxes.

Understanding these common mistakes can help you avoid them.

How a Simple System Changes the Way Agents Run Their Business

When you maintain a financial system consistently, several things begin to improve.

Financial clarity improves

Instead of guessing how your business is performing, you can review your income, expenses, and production at any time.

This helps you spot patterns.

For example, you may notice certain months tend to produce fewer closings, while other months consistently perform better.

Recognizing these trends helps you plan ahead and avoid unnecessary stress during slower periods.

Clear financial records can also prevent overconfidence during strong months, helping you maintain balance in how you manage your business.

Decision making becomes easier

Better information leads to better decisions.

When you can clearly see where your money is going, you can evaluate whether your investments are actually producing results.

For example, you may realize that one advertising channel generates very few leads while referral-based marketing produces your strongest clients.

Having reliable financial information allows you to adjust your strategy with confidence.

Tax preparation becomes far easier

For many agents, the biggest difference appears during tax season.

When financial records are organized throughout the year, preparing information for your accountant becomes simple.

For example, agents using LEDGNT can export their financial records with a single click during tax season. Instead of spending hours gathering receipts and reconstructing expenses, everything is already organized and ready to share.

This alone can save significant time and reduce the stress many agents experience each year when taxes are due.

Business confidence increases

Perhaps the most important benefit is confidence.

When your financial system is working, you are no longer guessing about your business.

You know what you’ve earned, what you’ve spent, and how your business is performing.

That clarity makes it much easier to operate like a professional business owner rather than feeling like you’re constantly trying to catch up.

A Simpler Way to Manage Real Estate Business Finances

Many agents assume they need complicated accounting software to stay organized.

In reality, most real estate agents simply need a system designed for the way their business operates.

That means having one place to track:

closings

expenses

mileage

Tools built specifically for real estate professionals can make this process much easier.

For example, some agents use LEDGNT, a financial tracking system designed specifically for real estate agents to organize closings, expenses, and mileage in one place.

Because the system focuses on the core financial activities of an agent’s business, it removes much of the complexity found in traditional accounting platforms.

Final Thoughts

Financial organization does not require complicated bookkeeping.

In most cases, real estate agents simply need a clear and consistent system for tracking the financial side of their business.

A simple financial system allows you to:

stay organized throughout the year

understand your business numbers

reduce tax season stress

operate more professionally

Once a system is in place, financial tracking becomes a small routine rather than a recurring problem.

Over time, that organization creates greater clarity, confidence, and control over your business.

Learn more about LEDGNT at: https://ledgnt.com

Subscribe to our Mailing List

Subscribe to be notified when new articles go live & receive helpful tips on running the financial side of your business.

RELATED ARTICLES

March 24, 2026

LEDGNT APP

Christian Tiessen

Christian is a financial strategist and the founder of LEDGNT, a platform designed to simplify financial tracking for real estate agents. He specializes in helping agents create clarity, organization, and consistency in their business finances.

LEDGNT is a financial tracking app built specifically for real estate agents to track closings, expenses, and mileage in one place.