WHY REAL ESTATE AGENTS NEED A FINANCIAL SYSTEM TO STAY ORGANIZED

Real estate agents need systems to stay organized. Learn how a simple financial system helps track closings, expenses, and mileage year-round.

03/08/2026 | 8 Minute Read

By: Christian Tiessen

Real estate agents spend most of their time focused on clients, showings, contracts, and closings. Financial tracking often becomes something that gets pushed aside until it absolutely has to be handled.

At first, this may not seem like a problem. But over time, small gaps in organization begin to build up.

Receipts end up in different places. Mileage gets forgotten. Closings are tracked inconsistently. Expenses are saved in emails or written down in notes that are difficult to find later.

Eventually everything starts to feel scattered.

Many agents only realize how disorganized their financial records have become when they suddenly need that information. What should be simple turns into hours of searching for receipts, reconstructing expenses, and trying to remember details from months ago.

A financial system solves this problem by creating consistent processes for tracking the financial side of your business.

If you want to understand the full framework many agents use, this guide explains the structure in detail:

The Complete Guide to Real Estate Agent Financial Systems

Systems Create Consistency

One of the most important ideas in business management is that systems create consistency.

In the classic business book The E-Myth Revisited, author Michael Gerber explains that successful businesses rely on documented systems rather than memory or individual effort.

Instead of depending on someone to remember what to do, a system creates a repeatable process.

This idea applies perfectly to real estate.

Many agents operate without clearly defined systems for parts of their business like:

lead generation

transaction management

marketing

financial tracking

Without systems, everything becomes reactive.

You track expenses when you remember.

You log mileage when you think about it.

You organize receipts when something forces you to.

But when you create a simple financial system, the process becomes consistent.

Expenses get recorded the same way every time.

Closings are logged in one place.

Mileage is tracked regularly.

Consistency is what turns financial tracking from a stressful task into a small routine.

Systems Allow Businesses To Improve Over Time

Another advantage of systems is that they make improvement possible.

When a process is documented, you can observe how it works and make adjustments over time.

For example, you might notice that your current method of storing receipts takes too long. Or you may realize that your mileage tracking process needs to be simplified so you actually maintain it consistently.

Without a defined system, these improvements are difficult to make because the process is constantly changing.

A system gives you something stable that can be refined over time.

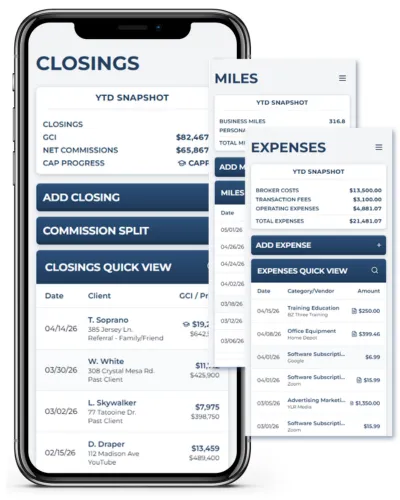

Many agents eventually reach a point where they decide to use a tool designed specifically for their workflow. For example, some agents adopt tools like LEDGNT, which allow them to track closings, expenses, and mileage in one organized place. Because everything follows the same structure, it becomes easier to maintain consistency week after week.

The key idea is not the tool itself, but the system behind it.

When the process is clear, improvement becomes natural.

Subscribe to our Mailing List

And that's just a peek at what we offer. Get more marketing tips straight to your inbox.

Without Systems, Everything Becomes Reactive

When financial tracking is not part of a defined system, agents tend to operate reactively.

Instead of maintaining records consistently, financial organization happens in bursts when it becomes unavoidable.

For example:

An agent might realize they haven’t logged expenses in several months and try to reconstruct everything from bank statements. Or they may attempt to calculate mileage long after appointments and showings have already happened.

These situations are stressful because the information was never captured when it occurred.

Systems prevent this problem by creating predictable routines.

A few minutes each week is usually enough to maintain a financial system that keeps everything current.

Without that system, financial tracking slowly falls behind until it becomes overwhelming.

Tax Season Reveals Broken Systems

Tax season is when many agents realize their financial tracking system is not working.

Suddenly they need:

a list of business expenses

mileage totals for the year

records of closings and commissions

documentation to support deductions

If these records have not been maintained throughout the year, agents often spend hours trying to reconstruct the information.

Receipts must be searched for.

Bank statements must be reviewed.

Old emails must be checked for missing expenses.

What could have taken minutes throughout the year turns into a stressful project.

The IRS requires accurate documentation for business deductions, including expenses and other records maintained by self-employed professionals.

This experience is often what motivates agents to finally implement a more reliable financial system.

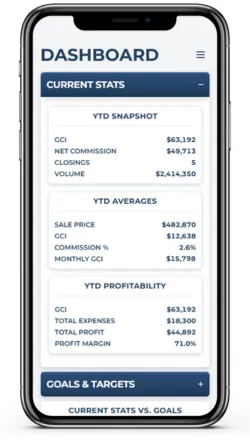

A Financial System Creates Clarity

A good financial system does not need to track dozens of complicated metrics.

For real estate agents, the financial side of the business comes down to three core areas:

Closings

Expenses

Mileage

When these three categories are tracked consistently, your entire business becomes easier to understand.

The LEDGNT app allows you to track these three areas in an easy to learn format. Watch the short demo video to see how it works!

Closings

Closings represent the production side of your real estate business.

Tracking closings allows you to see how many transactions you have completed, how much commission income you have generated, and how your production changes throughout the year.

Over time this data reveals patterns in your business. You may notice seasonal trends, production growth, or changes in transaction volume that help you better understand how your business operates.

Without a system, this information is often scattered or incomplete.

Expenses

Expenses reveal how much it costs to operate your real estate business.

Marketing campaigns, software tools, professional memberships, advertising, and office supplies all contribute to the cost of running your business.

When expenses are recorded consistently, you can quickly see where your money is going and evaluate whether those investments are producing results.

For example, you may discover that certain marketing channels consistently produce strong leads while others generate very little return.

Without organized expense tracking, these insights are much harder to see.

Mileage

Mileage is one of the most commonly missed deductions for real estate agents.

Showings, listing appointments, inspections, and property tours can add up to thousands of miles each year.

When mileage is tracked consistently, those miles can often be deducted as part of your business expenses. But if mileage is not recorded at the time the driving occurs, it becomes very difficult to reconstruct later.

A simple system ensures these miles are captured as they happen.

Organization Reduces Stress

When financial tracking becomes part of a consistent system, agents experience a noticeable shift in how they feel about their business.

Instead of wondering whether their records are complete, they know everything is documented.

Instead of scrambling to find receipts, they know exactly where they are stored.

Instead of avoiding financial tasks, they complete them quickly because the process is simple.

This sense of organization allows agents to focus more energy on the parts of their business they enjoy most: working with clients and closing deals.

A Simple System Makes The Entire Year Easier

The goal of a financial system is not to create more work. It is to eliminate friction.

Instead of trying to organize everything at the end of the year, agents maintain their system throughout the year in small, consistent steps. Expenses are recorded when they occur. Mileage is logged regularly. Closings are tracked in one organized location.

Because the information is always current, tax season becomes dramatically easier. There is no scrambling to reconstruct records or search for missing receipts. Everything is already documented.

More importantly, a consistent system provides clarity. You always know where your business finances stand, which allows you to run your real estate business with greater confidence and professionalism.

Many agents eventually move away from scattered spreadsheets and notes in favor of tools designed specifically for the way real estate businesses operate.

Systems like LEDGNT make it possible to track closings, expenses, and mileage in one organized place so financial tracking becomes a simple routine rather than a recurring problem.

Once the system is in place, maintaining it usually comes down to a few small routines each week.

When the system is clear and easy to maintain, financial organization stops feeling like a burden and becomes a small habit that supports a well-run real estate business.

Learn more about LEDGNT here: https://ledgnt.com

RELATED ARTICLES

March 24, 2026

LEDGNT APP

Christian Tiessen

Christian is a financial strategist and the founder of LEDGNT, a platform designed to simplify financial tracking for real estate agents. He specializes in helping agents create clarity, organization, and consistency in their business finances.

LEDGNT is a financial tracking app built specifically for real estate agents to track closings, expenses, and mileage in one place.